Earned vs. Unearned Tuition for Cosmetology Schools—Why It’s Required

Accredited cosmetology schools that receive Title IV funding are required to comply with specific financial reporting standards—especially when it comes to tuition revenue. One of the most misunderstood (and most audited) concepts in school accounting is the distinction between earned and unearned tuition.

This blog explains what these terms mean, why proper classification is essential for Title IV compliance, and how getting it wrong can lead to audit findings, negative composite scores, or worse—loss of accreditation.

What Is Earned vs. Unearned Tuition?

Earned tuition refers to the portion of tuition revenue a school has legitimately earned based on the amount of educational instruction delivered to the student.

Unearned tuition, on the other hand, is the portion of tuition that has been collected but relates to future instructional hours the student has not yet received.

Example:

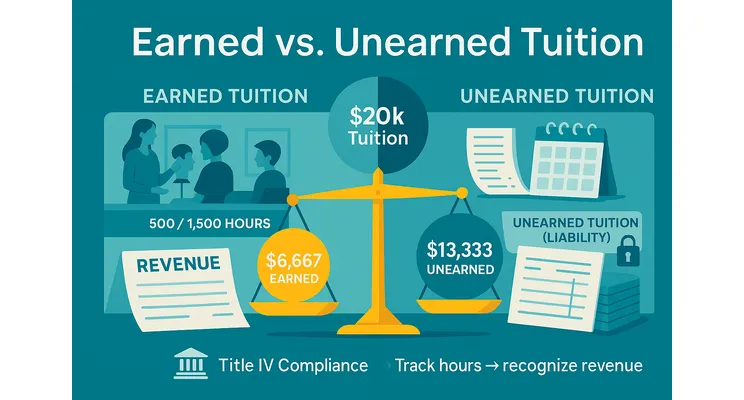

If a student pays $20,000 upfront for a 1,500-hour program, and the school has only delivered 500 hours as of the balance sheet date:

Earned tuition = $6,667

Unearned tuition = $13,333

Unearned tuition must be recorded as a liability, not income.

Why Unearned Tuition Is Required for Accredited Schools

Accreditation agencies like NACCAS and ACCSC—along with the U.S. Department of Education (ED)—require institutions to follow accrual basis accounting in accordance with GAAP (Generally Accepted Accounting Principles). This includes proper revenue recognition.

Here’s why:

1. Audit Requirement

Accreditation and Title IV audits test whether schools are recognizing revenue appropriately. If all collected tuition is recognized as revenue immediately, the school fails the compliance test. Auditors expect to see a clear breakdown of earned vs. unearned tuition in your trial balance and financials.

2. Composite Score Impact

Incorrect revenue recognition can inflate income, misrepresent net assets, and ultimately distort the Composite Score submitted to the ED. A failing score can put the school on Heightened Cash Monitoring (HCM) or worse, trigger financial responsibility reviews.

3. Student Refund Calculations

If a student withdraws, the school must calculate how much of the tuition is refundable based on hours attended. Without tracking unearned tuition, refund liability is often miscalculated—leading to findings.

Common Mistakes Schools Make

Treating all tuition as earned upon receipt

This is incorrect under GAAP and a red flag in audits.Not maintaining a liability account for unearned tuition

Schools should have a clearly labeled liability account (e.g., “Unearned Tuition Revenue”).Manual tracking in Excel with no supporting schedule

Auditors require supporting schedules that reconcile to the general ledger.Incorrect adjustments at year-end

Year-end journal entries must match the actual instruction hours delivered as of the reporting date.

What You Should Do

Implement Accrual-Based Revenue Recognition

Your books must reflect earned tuition based on the hours delivered. Unearned tuition must be carried as a liability.Maintain a Tuition Reconciliation Schedule

Use a spreadsheet or accounting system to track tuition by student and calculate earned vs. unearned monthly or quarterly.Train Your Accountant or Bookkeeper

Most CPAs and bookkeepers unfamiliar with Title IV accounting miss this critical requirement. Ensure your financial professional understands DOE and accreditation standards.Review Your General Ledger

Look for tuition revenue accounts and confirm you also see an “Unearned Tuition” liability. If not, you likely need a correction.

Final Thoughts: It’s Not Optional

For Title IV schools, tracking unearned tuition isn’t a best practice—it’s a requirement. Failing to comply can result in audit findings, demands for financial aid reimbursement, or, in extreme cases, loss of accreditation.

At CAP Academy, we specialize in helping cosmetology schools build audit-ready books that comply with Title IV, NACCAS, and ACCSC requirements. Whether you’re fully accredited or just starting the process, understanding your unearned tuition liability is the foundation of financial compliance.

Learn more about our Cosmetology Audit Prep Academy (Cap Academy) — where we prepare accredited schools for audit success.